Using the Relative Value Units (RVU) method

The Relative Value Units cost allocation method is the most commonly chosen methodology in which to calculate cost at the cost item level. RVUs were developed in the late 1980s from Harvard University study of physicians estimates of the work involved in providing their services in comparison to work involved for particular services. The results of these estimates evolved into the RVUs used for services today.

RVUs allow you to assign a measure of relative comparison value to the items to be costed, and then based on the RVU value of the cost item, allows you to determine the cost item's cost. In costing, RVUs are created for various types of costs but typically come in the form of labor minutes, which are used to allocate cost from labor cost pools, or an acquisition cost, which is used to allocate from supply cost pools.

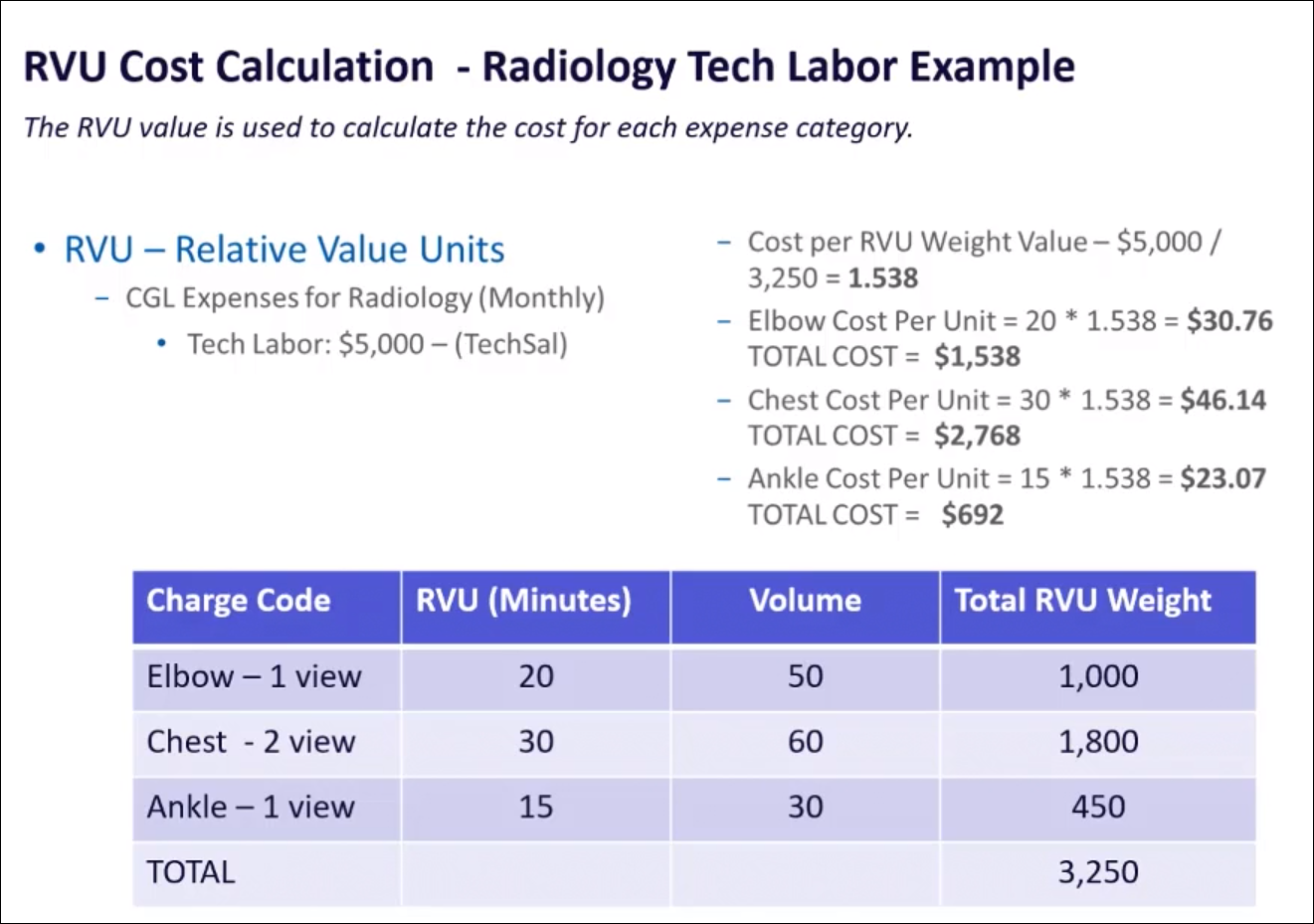

In the following example, the radiology department has $5,000 in technician labor expenses. This department has three study-type charges: Elbow 1, Chest 2, and Ankle 2. The department uses the minutes it takes to do each study as the RVU value for each study. The RVU value is multiplied by its volume to calculate the total RVU weight. The sum of the RVU weight for all three charges is $3,250. The total RVU weight is used to calculate the technician cost for each charge. The technician labor cost is divided by the total RVU weight to calculate the cost per RVU weight value, which in the following example is 1.538.

The elbow charge cost per unit is the elbow view 20 RVU multiplied by 1.538 to equal $30.76. With a volume of 50, the total is $1,538. The same calculation methodology is also applied to the chest and ankle studies.

Example of how RVU is calculated for a department

RVUs are assigned to cost items within a department and entity for a facility or a provider. This allows codes to receive only the related expenses, such as labor for time charges and supply expense for implant items. The RVU basis should reflect the department structure and data available.

You should update RVUs, as needed. For example, when minutes are used for procedures, you should check in once a year with the department managers to verify whether or not anything has changed. Have they made processes changes that have made some procedures quicker or is there no longer a need for an RN to be present for certain procedures? Have any procedures been added? Setting up an annual review of RVUs is a best practice you should use to make sure that you are allocating costs properly.

TIP: The most basic rule of RVU costing is that any item that does not consume resources should receive an RVU value of zero so that no cost is assigned to that cost item.

RVU vs RCC method

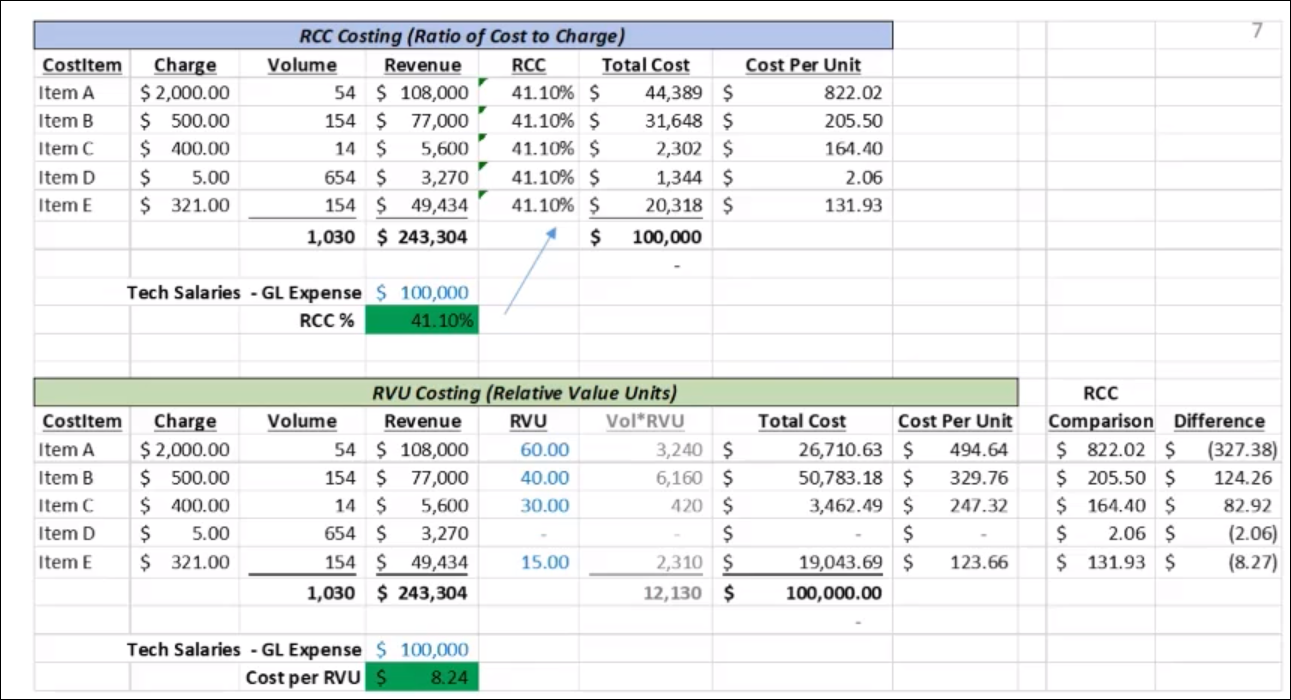

Both the RVU and Ratio-to-Cost (RCC) methods are both allocation cost methods—meaning that all of the expenses in the department are used to calculate the cost of the cost items. In RCC, that ratio of cost to charge is calculated based on the revenue and expenses of the cost category. In the following example, the total revenue of all the cost items is $243,304 and the expenses for the technicians is $100,000. The RCC is 41.10%. That RCC is used to calculate the cost of the cost item.

Comparison of cost calculations between RCC and RVU methods

For RVU, the total weighted RVU volume and the expenses for the technician salaries are used to calculate a cost per RVU, which is $8.24. This cost per RVU is used to calculate the unit cost of the item. When you compare the RCC cost results to the RVU cost results, you can see that the RVU value drives the cost per unit. If an item does not have an RVU value, Axiom will not calculate a cost per unit.

The RVU cost method is a more accurate cost method than RCC because it does not depend on the price of an item to calculate the cost.

Best practices for collecting RVUs

The following process describes a general procedure to gather the information you need to determine RVUs.

-

Determine the department(s) in which to collect the RVUs.

-

Set up meetings with department managers to discuss the process and the benefits of using RVUs in costing. It is likely that you will need to have more than one meeting. If possible, have a meeting with all of the department leaders of a particular service line at the same time. For example, all radiology or pharmacy. If you are a multi-facility organization, plan to bring together someone from each facility to participate.

-

Collect revenue and usage data on each department that is relative to the time period that is being costed. Revenue and usage data contains a list of cost items (charges, procedures, etc.) along with volume and unit charge that are captured within that department.

-

Set up a spreadsheet for each department that lists the cost items vertically, with the volume, revenue, unit charge, and all cost categories used in that department in columns.

-

Discuss departmental operations.

-

Discuss the staff and their roles within the department: RN, Tech, Managers/Supervisors, etc.

-

Walk through the process of servicing an average patient who has a visit in this department:

-

How does the patient arrive to the department? Are they transported by the transport department, or does someone from this department retrieve the patient from their room or other area? Is this an outpatient department where the patient arrives without assistance?

-

Is registration involved? Who registers the patient?

-

Is pre-procedure work completed? Who performs this work? Is it performed prior to arriving to this department?

-

Who performs each function and how long does it take? How many procedures are charged to the patients in this department? Does an RN take 10 minutes, 20, or not involved at all with specific procedures? How about the tech or aide? Or perhaps all are involved but for different lengths of time.

NOTE: For multi-facility organizations, there will be nuances that will dictate differences in RVU collection. For example, a larger hospital may have a transport department that moves patients around to where their next test is located, but the small hospital has to send staff to retrieve the patient from their room. The time it takes to perform a task in the hospital with the transport department will be less than the hospital who has to get the patient. There may be small hospitals, however, who bring the equipment to the bedside and may actually take less time than the larger hospital. The goal is to understand the process involved within each department for an average case and to determine the skill mix and time needed to perform procedures.

-

-

Collect supply, pharmacy, depreciation, and other RVUs based on various measures, which may or may not involve a measure of time. Supplies are typically acquisition cost (microcosted), as is pharmacy. Depreciation is typically fixed asset information, all of which are a separate function from the traditional RVU process in Axiom Enterprise Decision Support.

-