Understanding cost accounting

What is cost accounting?

At its most basic level, cost accounting allows you to assess the cost or value of a product or service. Determining the cost of various components that comprise an end-product is useful for price setting, cost control, negotiations, and analytics. Cost accounting may involve different techniques, depending on the industry.

In healthcare organizations, cost accounting is used to determine the cost of each service or product used in patient care, providing detailed information that can be used for analytics and decision-making.

For example, the cost of an x-ray includes labor, supplies, depreciation, and overhead. Combined with other charges on a patient’s transaction record, a complete picture of a patient visit emerges. The data can be compared to payer rates to determine whether costs are in line with expected reimbursement to make pricing decisions. The same data can be parsed a different way, aggregated by provider, for example, to assess the provider’s performance against peers. Cost data is also useful in facilitating staffing decisions, informing capital request decisions, exploring new services, and more.

What is cost accounting used for?

Organizations use cost accounting data for many purposes. Understanding the underlying cost of the products and services produced allows an organization to review and assess financial performance at a granular (per unit) level and a higher level (product line, location, or other classification). Cost results can be used to assess or set prices. Knowing detailed cost results enables more successful contract negotiations—with vendors, contractors, and providers. Costing knowledge also brings informed decision-making at both the tactical and strategic levels.

What are the advantages of cost accounting?

Without cost accounting, organizations are left with two options—relying on general ledger data or homegrown “back-of-the-envelope” analytics. Both approaches to decision-making are risky.

While general ledger represents a true cost, the detail level is too high for informed decision-making. Department and account data often lack the nuance of quantity and cost per unit spread across many units. Rudimentary analytics using Excel can be error-prone and subject to the whims of the person performing the calculations.

Cost accounting determines an accurate cost per unit broken out by cost categories (labor, supplies, capital, etc.), thus enabling aggregation at meaningful levels. The methodology applies mathematical principles and technology to calculations to ensure accuracy, repeatability, and reliability.

Why do organizations allocate indirect costs?

Many of an organization’s costs are indirect, not directly tied to the product or service but important to capture to make accurate pricing decisions. In the case of healthcare, indirect costs support direct patient care activities. Examples include accounting, collections, human resources, and IT. To fully cost patient activity, these indirect departments allocate their costs using meaningful statistics through the cost accounting process.

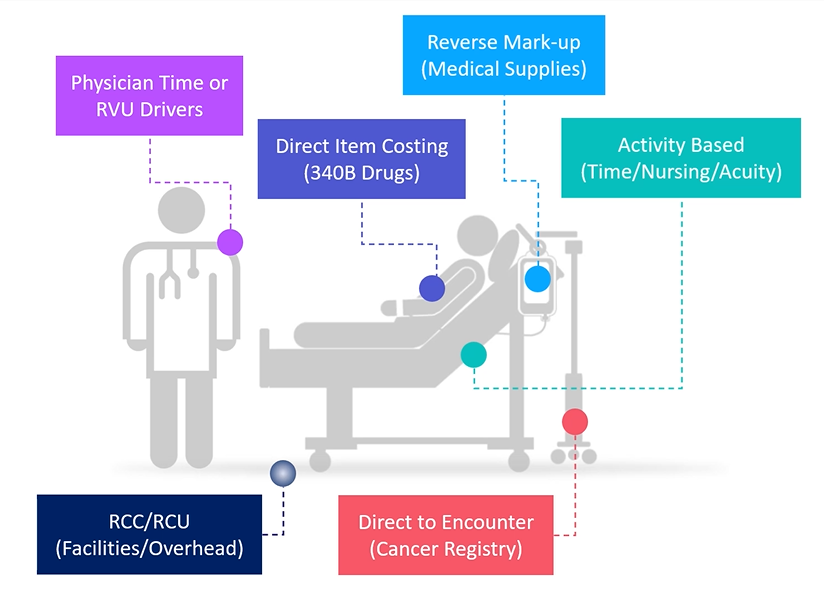

Which method of cost accounting is used in hospitals?

The following is a list of the different costing methods used by healthcare organizations"

-

Ratio of Cost to Charge (RCC) spreads general ledger (GL) costs across a set of service items in a department. While simple to maintain, RCC can lead to inaccurate results in instances where the prices do not align with resource utilization.

-

Relative Value Unit (RVU) also spreads GL dollars in the department, but the basis is a value that indicates relative resource utilization. Organizations that have a reliable process for keeping RVUs up to date get more accurate cost results.

-

Microcosting assigns the actual vendor cost of items when that data is available. Or they back into this cost if the markup rates are available.

-

Direct Costing, or activity-based costing, is helpful for labor costs when the resource use and the average hourly rate are known. This approach can also be used for indirect costs that directly impact patient care. These direct and activity-based costing approaches are accurate and create a high degree of confidence in the resulting cost data.

Healthcare costing methods

In addition to how an organization treats indirect cost, there are several methods to consider for calculating the cost per unit. This decision point is, in some ways, the more critical focus when designing a costing system or responding to a major organization initiative. When selecting a cost method, consider the type of item being costed, the resources available for the cost calculation, and the accuracy desired in the results. Cost items are typically chargemaster (CDM) codes but can also be items such as CPT codes or the pseudo cost items created through the direct-to-encounter utility.

Traditional costing approaches include Ratio of Cost to Charge (RCC), Relative Value Unit (RVU), and Relative Cost Unit (RCU). These methods are well-known and frequently used in the healthcare industry. These more basic methods can be used for indirect costs, areas where scrutiny of results is less of a focal point, or where resources are limited in some way.

Advanced costing methods

There are two advanced cost calculation methods to consider as well: micro-costing and reverse markup. With micro-costing, the vendor cost can be assigned directly to the cost items or to the actual transaction level for encounters. This highly accurate approach increases transparency and buy-in. The source data from vendors is the assigned cost, and a resulting variance to the general ledger can be included or excluded from the cost process. When possible, assigning this vendor cost at the actual encounter transaction level (transaction microcosting) is highly recommended. A data feed with the vendor cost is required to enable this method for large groups of cost items.

Using the reverse markup method, an organization can leverage its markup policy to back into the vendor cost when the vendor cost is unknown. This method is not as accurate as micro-costing but does offer efficiency since it requires less maintenance and no detailed data feeds. In addition to these advanced methods, an expansion of basic RVUs to the more strategic areas of focus can be leveraged to increase accuracy and reliability of the RVU approach. This expansion should include detailed time-and-motion studies at the charge item level to ensure reliable results.

Timing options for cost modeling

Given the significant business disruption of COVID-19 and impacts on both volumes and costs, cost modeling will not follow normal trends and will have continuing downstream impacts on reporting. Syntellis’ Axiom Enterprise Decision Support supports a variety of costing approaches and methodologies designed to more precisely attribute costs to patient care activities.

While new methodologies are being introduced to support more granular encounter-specific costs into the cost model, a significantly higher amount of direct patient care and overhead cost is being assigned to a cost item level in a cost-per-unit calculation. The goal is to ensure that the trending and ability to analyze cost is accurate and reflects the cost of providing care during each phase of the crisis and recovery. To this end, Axiom Enterprise Decision Support offers several options for the timing of cost calculations. Each option has different implications for encounter reporting.

Year-to-date costing

Calculated cost is stored for the full year-to-date (YTD) period, recomputed with each costing run for YTD costing; per-unit costs by cost item and cost category are computed each period using YTD dollars and volumes. For example, if you run costing for nine months, the system would calculate the cost as an average over the full nine-month period and store this in the resulting cost set. These values would then be assigned to all encounters in that nine-month period at the cost item level. This approach can be processed monthly, quarterly, or annually using the cumulative proceeding months.

Reporting implications: This method provides a consistent per-unit cost across time periods, which can be used to identify cost trends or utilization variation at a cohort or across physicians. Because the per-unit cost is constant, the differences in costs within the time period can be attributed to shifts in utilization and not unit cost rates. The disadvantage to this approach is that any cost shifts occurring at an operational level are averaged and are not highlighted in any given period, thus negatively impacting true trending of cost fluctuations.

Monthly costing

Calculated cost is stored uniquely for each month. For monthly costing, per-unit costs by cost item and cost category are computed each month based on the volumes and dollars for that specific period and stored specific to that month in a unique cost set. This enables detailed trending of the cost changes over months.

Reporting implications: If the goal of encounter reporting is to best capture how costs are shifting operationally from period to period, this method is preferable over the YTD costing process, as resulting encounter costs would capture those period-specific rates and changes.

Quarterly costing

Calculated cost is stored for each quarter. The quarterly costing option is similar to the monthly option but computes and stores unit costs using quarterly volumes and dollars, resulting in four values of cost for each fiscal year, all stored in unique cost sets.

The differentiator for monthly vs quarterly costing is how often the team has to run cost vs the quantity of updates to the configuration for new departments, accounts, and job codes. There is also a small learning curve that occurs when only run quarterly, especially if the cost analyst is doing other work in between cycles.

Reporting implications: Similar to the monthly option, quarterly costing captures some of the cost shifts that occur during the year yet provides some smoothing of the costs like the YTD option.