Working with Markup Groups

Markups are generally applied to supply items that have a variable cost to them based on the time and type of purchase. For example, all pacemakers may use the same cost item number, but the prices can vary by tens of thousands of dollars based on type and manufacturer as well as any purchasing agreements in place. Instead of a fixed charge, your organization uses a markup from the base cost to price the item in a way that ensures that they do not lose money on a consumable item.

The amount or percentage an item is marked up is determined using a markup table (referred to as a markup group in Axiom Cost Accounting). There are two methods you can use to apply markups: percentage or multiplier.

NOTE: Refer to your organization to determine which one to use when defining markups.

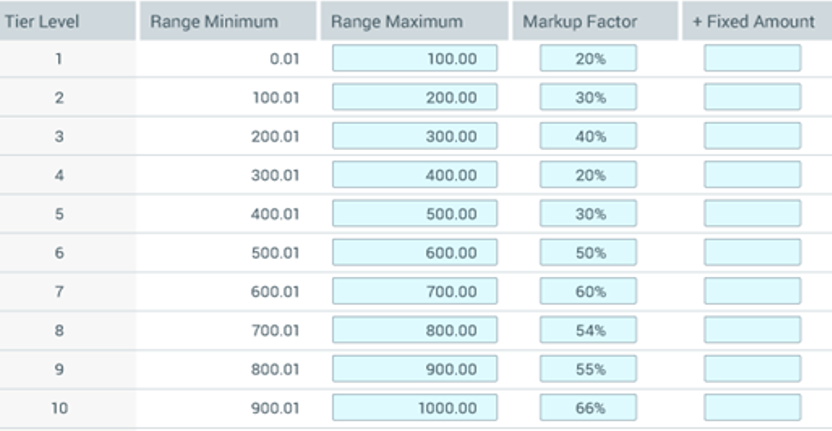

In Axiom Cost Accounting, a markup group consists of multiple pricing tiers, with each tier encompassing a price range and a markup percentage or multiplier that is added to the items in that price range. In the following example, a Supply markup group includes ten tiers that uses a percentage markup type, so items from $.01 to $100 are charged a 20% markup, $100.01 to $200 are charged a 30% markup and so on.

Reverse Markup method and unit costs

When using the Reverse Markup method, unit costs are calculated by taking the price of an item and marking it down based on the original markup percentage or multiplier defined in the markup group in which the item falls. Basically, you are reverse engineering the current price to determine the unit cost.

To illustrate the math, consider the following example:

- A $1,000 item falls into a tier that carries a 4.0 multiplier (some refer to this a 400% markup, please verify for your specific organization) from the base cost.

- The markdown rate would be: 1 / 400% → 1 / 4.00 → 1/4 → .25

- The original cost of the item would then be computed as: $1,000 * .25 = $250

- You can check this by reapplying the markup rate: $250 * Multiplier → $250 * 4.0 = $1,000

NOTE: Please check with your Kaufman Hall Implementation Consultant or with Kaufman Hall Customer Success for any questions about the computation of markup percentages or the differences between a markup percentage and a markup multiplier.

The Reverse Markup assignment results in either a remainder or an overage of dollars (or negative dollars) that is applied during the next methods based on methods assigned to other cost items. If no other methods are assigned or no other cost items are remaining, the balance is left on the GL as a variance. Each Cost Category could have its own markup table, which you should assign to the corresponding departments and cost categories.

To maintain markup groups for departments, do the following:

- Identify the cost items, cost pools, or entity/department combinations that you will assign to use the Reverse Markup costing method.

- Determine with department leaders and the Supply/Materials Management department the most appropriate costing method for medical supplies, implants, and pharmaceuticals.

- Obtain the markup tables from the CDM department. Departments that would commonly use a markup table would be Surgery, Cardiac Cath Lab, Ambulatory Surgery Centers, and the Pharmacy. Also consider Cost Items within departments that use large amounts of medical supplies, implants, or pharmaceuticals.

Markup group versions

Axiom Cost Accounting allows you to create a version of your markup groups as market conditions change. Each version includes all markup groups. You can then keep your markup tiers current without losing your historical settings should you ever need to rerun costing for a prior period of time. This allows you to update your tier structures without needing to update your Method Definition table version.